Payroll Services

A Simple Guide to Managing Your Restaurant Payroll

If you are an owner in the restaurant and hospitality industry, you may already know that restaurant payroll operates differently

If you are an owner in the restaurant and hospitality industry, you may already know that restaurant payroll operates differently

Managing payroll is a crucial aspect of running a small business. Ensuring employees are paid accurately and on time not

Do you know the tax implications of a company car? We can explain the impact of a company car on

Are you aware of the personal taxes you’re liable for as a company director? We’ve got the lowdown on self-assessment

Are you in the dark when it comes to business taxes? We’ve got the lowdown on the key taxes your

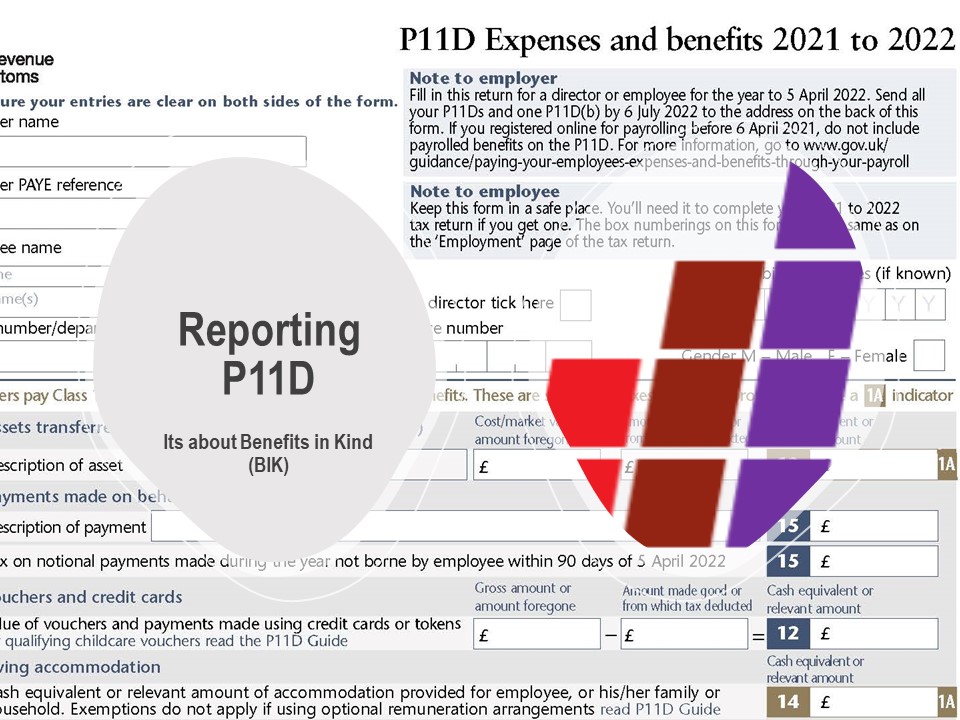

You might give a wide range of employee benefits outside of the salary and those benefits in kind could be